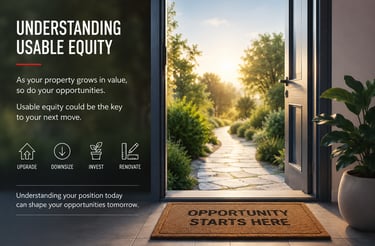

Understanding Usable Equity

Most homeowners understand that their property may have increased in value over time.

What many people do not fully understand is that this growth may have also created something called usable equity — and that usable equity may potentially open doors to opportunities that previously felt out of reach.

What Is Equity?

In simple terms, equity is the difference between:

what your property is worth today,

and what you still owe on your mortgage.

For example:

If your property is worth:

$800,000

And your remaining mortgage is:

$300,000

Your total equity would be approximately:

In this example, the homeowner may hold approximately $500,000 in total equity.

What Is “Usable” Equity?

Not all equity is automatically accessible.

Most lenders will generally only allow borrowing up to a certain percentage of the property’s value without additional lending requirements or lender’s mortgage insurance.

This is where usable equity comes in.

A common benchmark many lenders work around is 80% Loan-to-Value Ratio (LVR).

For example:

If a property is worth:

$800,000

80% of the property value would be:

If the remaining mortgage is:

$300,000

Potential usable equity may be approximately:

In this example, the homeowner may potentially have access to approximately $340,000 in usable equity, subject to lender approval and financial position.

Why Does This Matter?

Over the past several years, many property owners across Bundaberg and other parts of Australia have experienced significant property value growth.

As a result, many homeowners may now be in a much stronger position than they realise.

For some people, this may create opportunities to:

upgrade into a larger home,

downsize and reduce debt,

purchase an investment property,

renovate or improve their current home,

create additional financial flexibility,

or reposition themselves for the future.

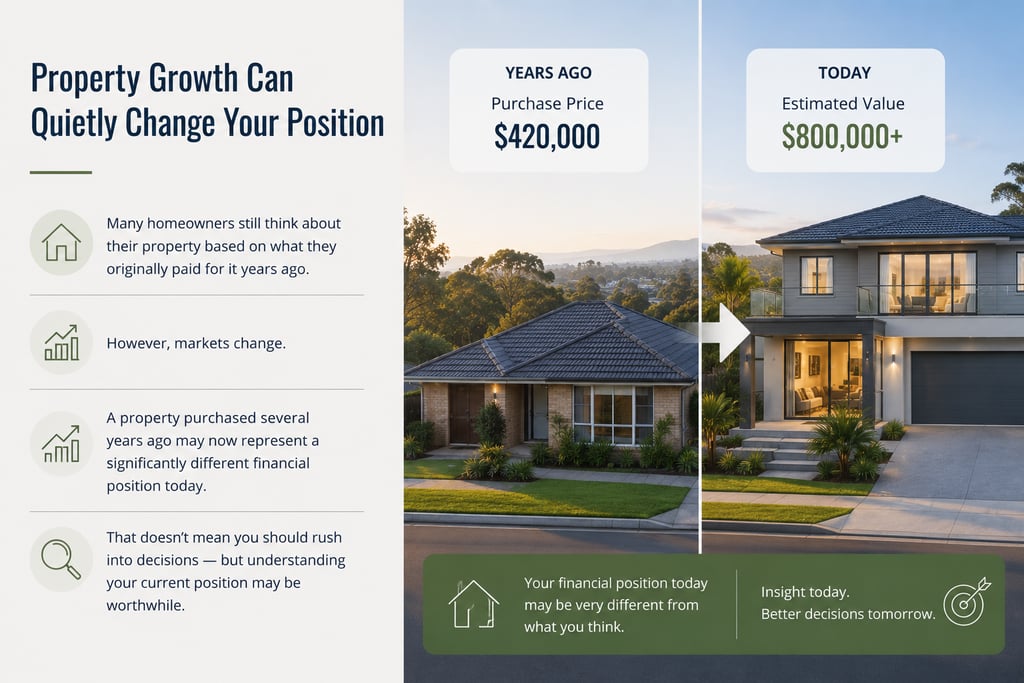

Property Growth Can Quietly Change Your Position

One of the most common things we see is homeowners still thinking about their property based on what they originally paid for it years ago.

However, markets change.

A property purchased several years ago may now represent a significantly different financial position today.

That does not necessarily mean people should rush into making decisions — but it does mean understanding your current position may be worthwhile.

Property Decisions Should Be Strategic

Usable equity is not about “maximising debt.”

In many cases, the smarter approach is about:

improving flexibility,

reducing financial pressure,

creating opportunity,

and making informed long-term decisions.

Every homeowner’s situation is different.

The important part is understanding what options may now exist.

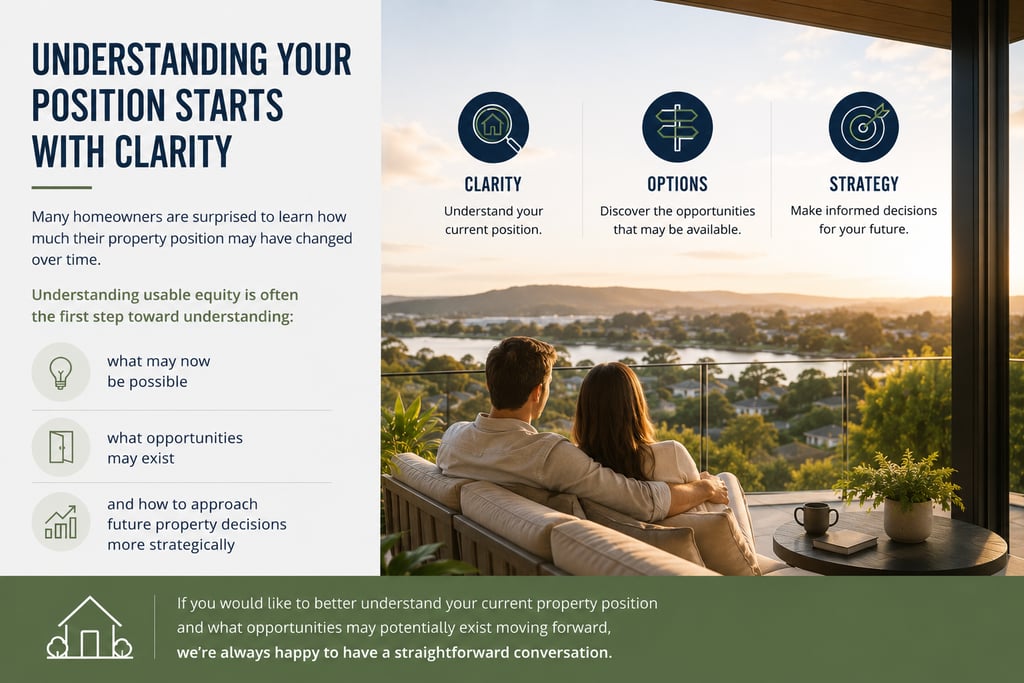

Understanding Your Position Starts With Clarity

Many homeowners are surprised to learn how much their property position may have changed over time.

Understanding usable equity is often the first step toward understanding:

what may now be possible,

what opportunities may exist,

and how to approach future property decisions more strategically.

If you would like to better understand your current property position and what opportunities may potentially exist moving forward, we’re always happy to have a straightforward conversation.